Packaging strategies are converging in ambition but diverging in execution. Both European and US brand owners face mounting pressures: rising costs, evolving consumer expectations and intensifying regulatory scrutiny. Yet how they respond to these challenges — and the strategic bets they’re making in 2025 — differs in meaningful ways.

L.E.K. Consulting’s latest proprietary brand owner packaging studies in Europe and the US reveal critical contrasts in investment priorities, sustainability expectations and cost management tactics.

Across a combined 1,000+ respondents that either directly or indirectly make decisions about packaging purchasing (brand managers, packaging designers, procurement, etc.), the data shows that while innovation and sustainability remain top of mind, regional context is shaping how brand owners translate these goals into action.

This article, the final in our four-part series, examines the key differences (and a few important similarities) between European and US packaging agendas in 2025.

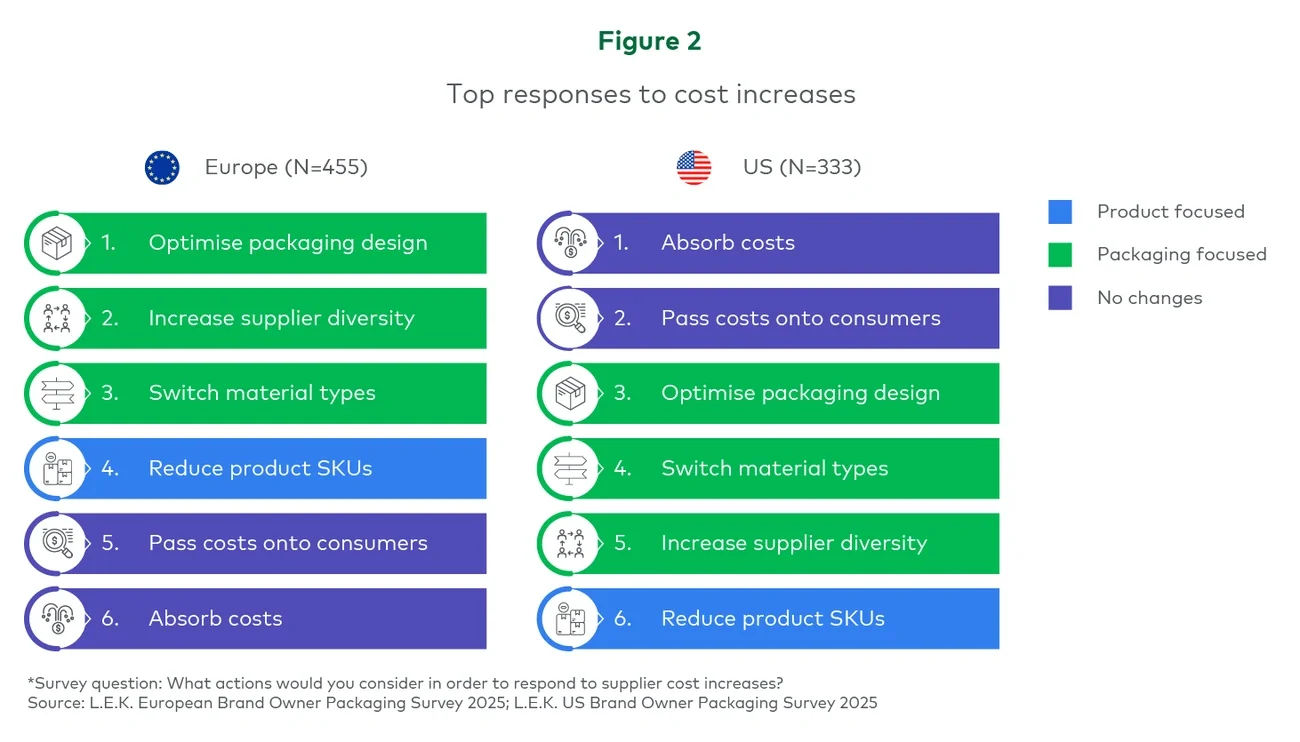

Cost pressure, different playbooks

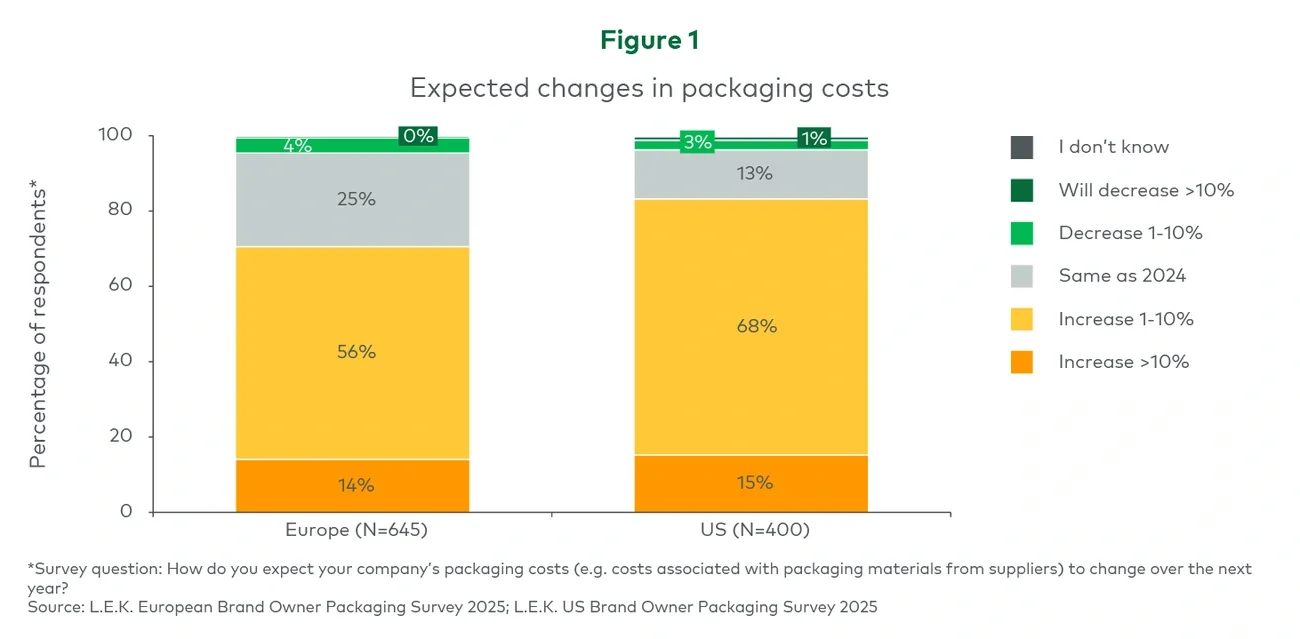

Both European and US brand owners anticipate higher packaging costs in 2025. But while 70% of European brands expect increases, the figure rises to 83% among their US counterparts (see Figure 1).