Agricultural growers have a variety of ways to source their inputs, including from established retailers, co-ops and distributors, as well as directly from manufacturers. But according to a survey L.E.K. Consulting conducted in February 2025, they are increasingly buying select crop inputs directly from manufacturers as they look to find the best prices available for key inputs. Many also report that they expect to continue doing so going forward.

Those are just a few of the key findings of our survey, which comprised more than 200 U.S. growers across a broad range of demographics and farm characteristics.

Survey respondent distribution:

Category | Subcategory | Percentage |

|---|---|---|

| Region | Northeast | 8% |

West | 20% | |

South | 28% | |

Midwest | 48% | |

| Crop type | Specialty crops | 20% |

Row crops* | 80% | |

| Farm size | 1,000-2,000 acres | 34% |

2,000-5,000 acres | 34% | |

5,000+ acres | 32% |

*Larger farms tend to skew slightly more toward row crop production.

As our findings make clear, the market for crop inputs is changing, with repercussions for channel players on the one hand and input manufacturers on the other. In order to stay competitive, both should be evaluating how they go to market and making any necessary adjustments.

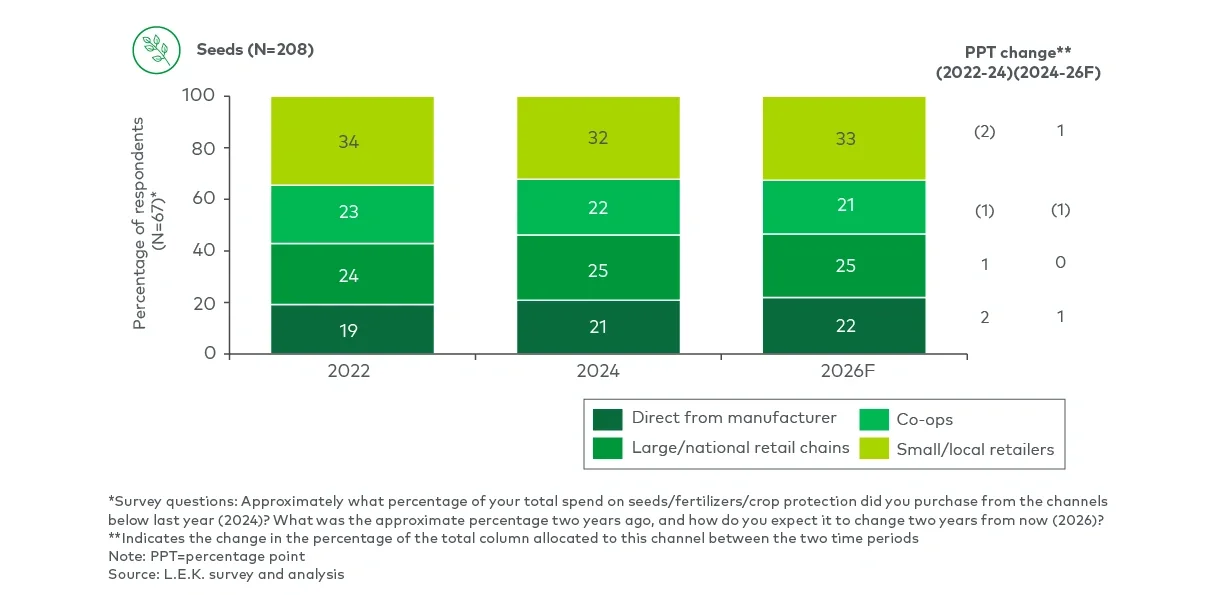

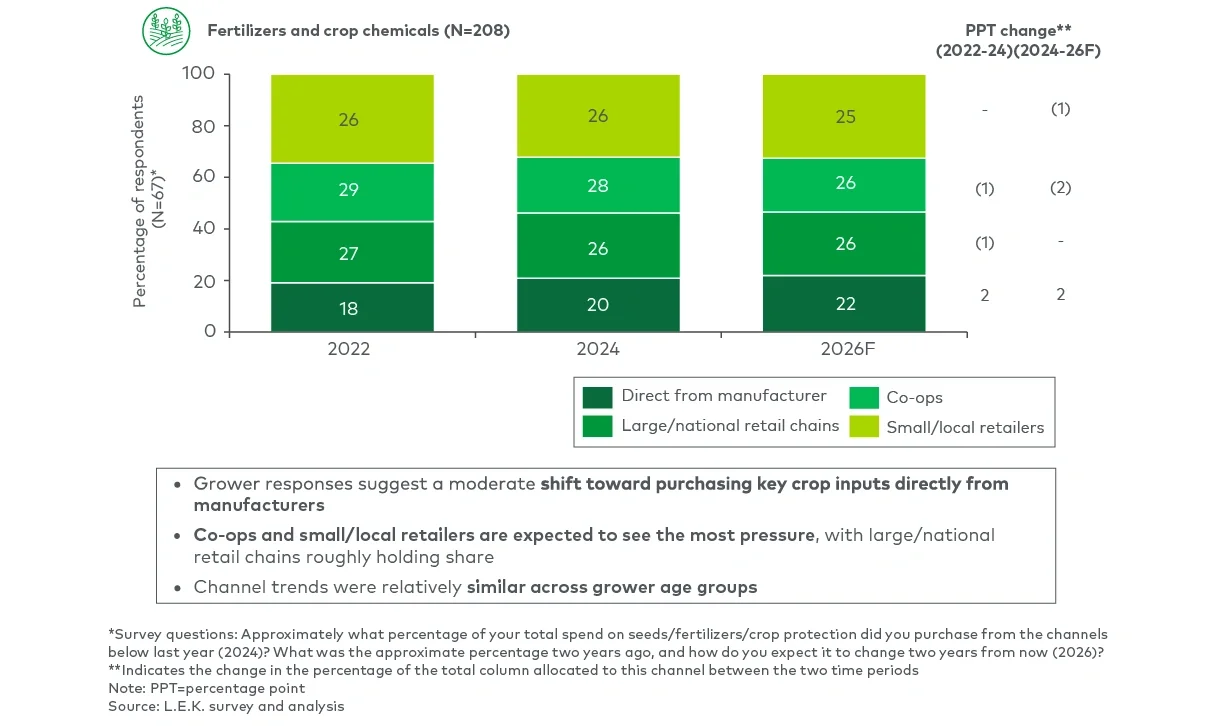

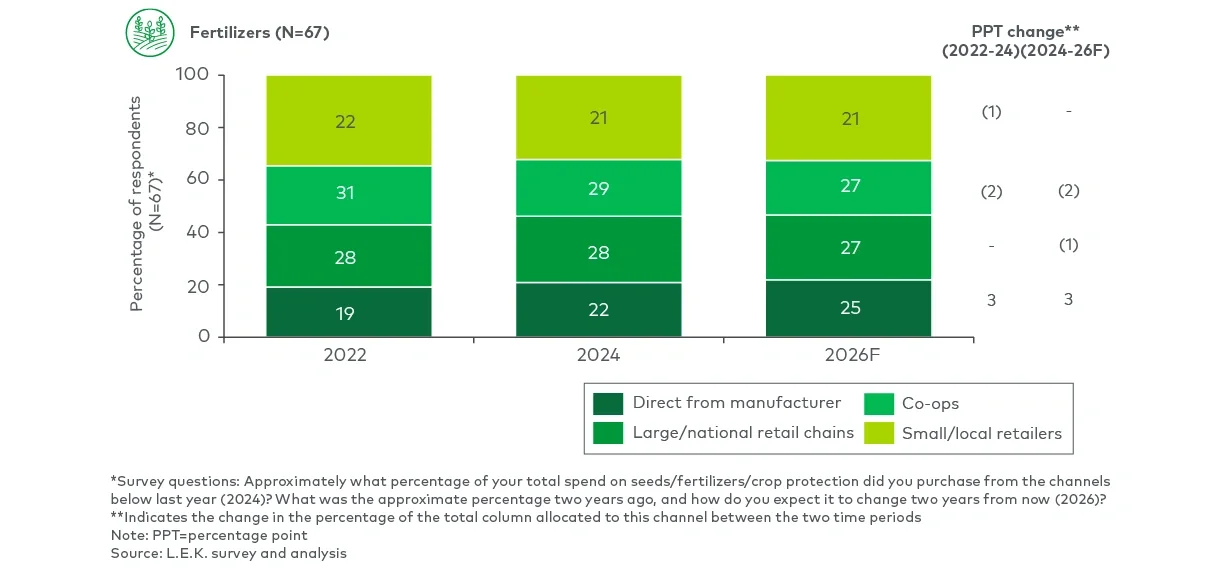

Growers are increasingly buying direct

A small but significant shift appears to be taking hold whereby an increasing share of growers are buying their seeds, fertilizers and crop chemicals directly from manufacturers. Grower responses suggest that number rose by approximately 2 percentage points from 2022 to 2024, to 21% from 19% for seeds and to 20% from 18% for fertilizers, and it’s expected to rise even further through 2026, to 22% for both (see Figures 1a and 1b).