As consumer needs evolve and brand expectations rise, CDMOs serving the nutritional supplements and beauty sectors are adapting to meet these shifting demands — from format expansion and broader service offerings to regional specialization and deeper capability sets.

L.E.K. Consulting’s proprietary CDMO database, “CDMOlodex,” tracks capabilities, services and specialization across hundreds of nutrition and beauty CDMOs in North America and Europe. These competitive dynamics provide critical context for investors and operators evaluating where the market is headed and how to identify winning platforms.

Positive tailwinds for the CDMO sector

There are several macro factors driving the attractiveness of this market:

- Large and growing markets: Nutrition and beauty categories continue to experience steady mid-single-digit growth driven by sustained consumer demand.

- Recession-resilient segments: These categories have proven durable during economic downturns — for example, according to the Nutrition Business Journal, nutritional supplement sales grew roughly 6% annually during the global financial crisis of 2007-2009.

- Indexed access to attractive categories: CDMOs offer a way to participate in the long-term growth of the nutrition and beauty markets without exposure to the volatility or life cycle risk of individual consumer brands.

- Increase in outsourcing: Brands are increasingly turning to CDMOs to manage complexity, reduce regulatory burden and increase speed to market with innovation.

- Sticky customer relationships: CDMOs benefit from recurring revenue streams and usually sticky customer relationships — though customer concentration and evolving brand strategies can present ongoing risks.

- Fragmented market with consolidation potential: The sector remains highly fragmented, with opportunities for roll-ups and platform creation.

What the data tells us: Trends from the front lines

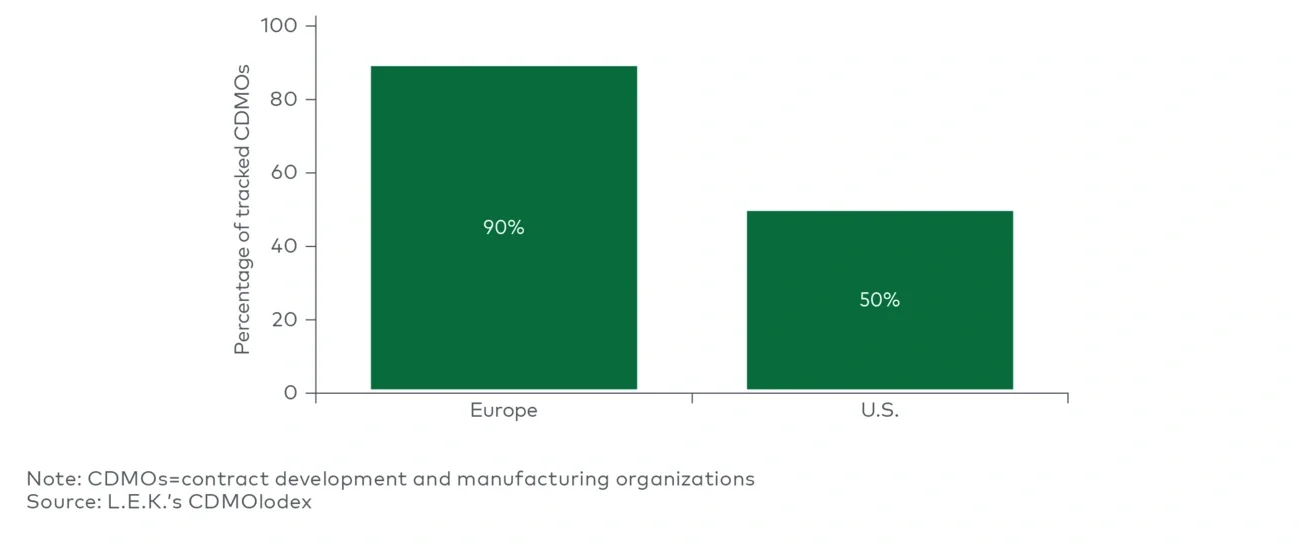

To better understand how CDMOs are evolving — and where the strongest opportunities lie — we analyzed data from CDMOlodex. The data reveals clear shifts in format expansion, capability development and regional specialization.

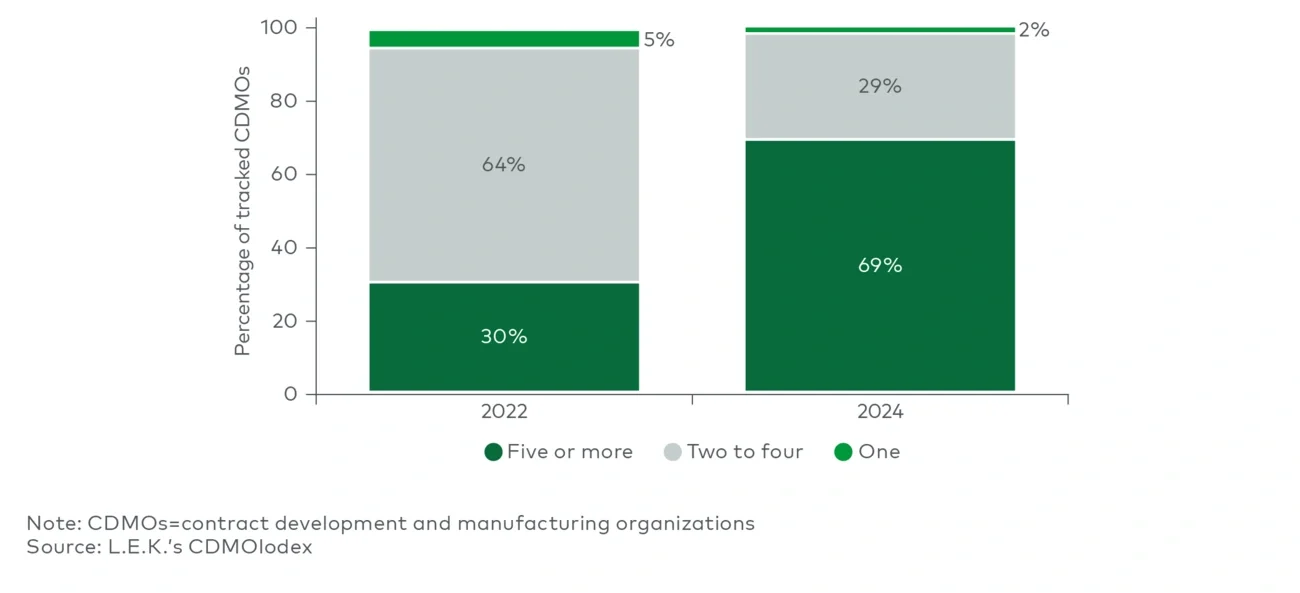

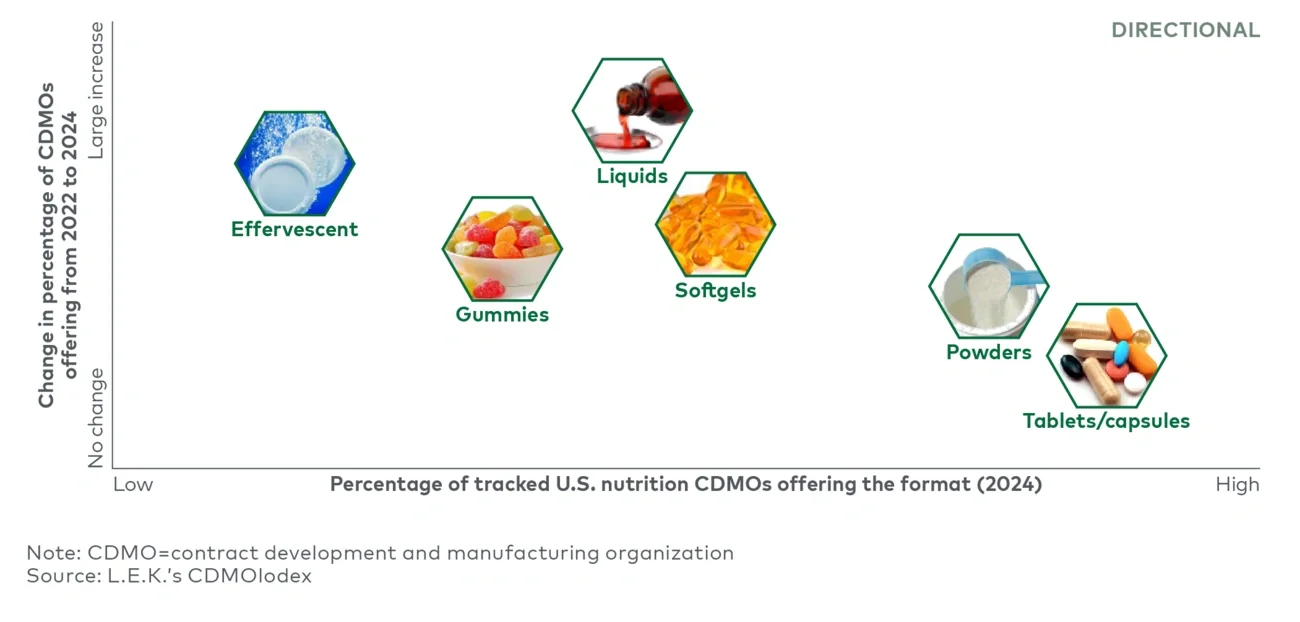

The rise of one-stop shops

To meet expanding brand demands, CDMOs are increasingly positioning themselves as one-stop shops — broadening their capabilities to serve a wider range of product types and services. This breadth allows CDMOs to grow share of wallet with existing customers by supporting more formats across the product portfolio. This increasing breadth is particularly evident in nutrition, where the share of U.S. CDMOs offering five or more formats jumped from approximately 30% to about 70% between 2022 and 2024 (see Figure 1).